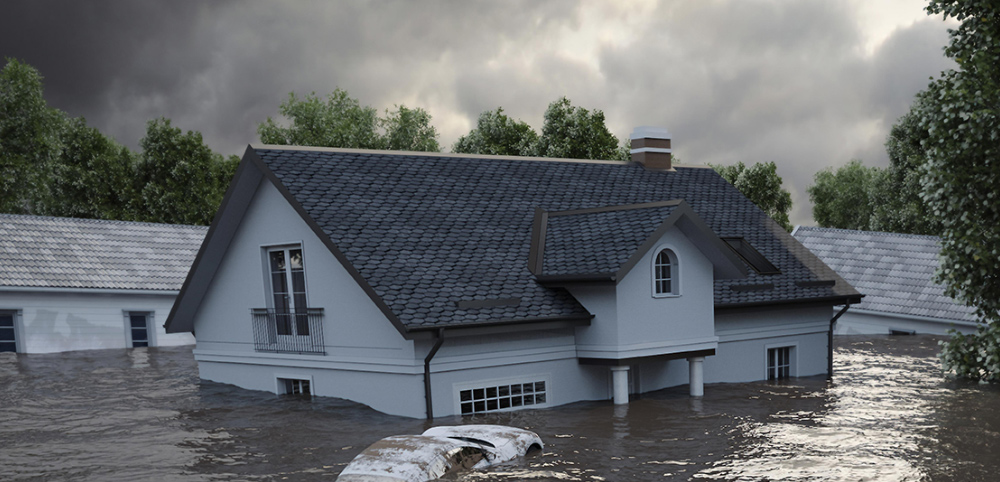

MIAMI – Sharp increases in federal flood insurance rates are distressing coastal homeowners from Hawaii to New England and are starting to hurt property values and housing sales in areas just beginning to recover from the recession, according to residents and legislators.

In recent weeks, the hefty flood insurance rate increases brought about by a 2012 law have stoked widespread alarm and uncertainty, prompting rallies, petitions and concern among state governors. Mississippi has sued the federal government to try to block the law. The issue has even garnered the attention of lawmakers, otherwise mired in the acrimonious government shutdown. A bipartisan group of senators and House members from Gulf Coast states are pressing for significant adjustments to the law once the Capitol returns to normal.

The law, officially known as the Biggert-Waters Flood Insurance Reform Act, is being rolled out in stages, with a major part having gone into effect on Oct 1. It removes subsidies that keep federal flood insurance premiums artificially low for more than a million policy holders around the country – a discount that was applied to properties that existed before the drawing of flood insurance rate maps.

An estimated 20 percent of the property owners with federal flood insurance received these subsidies as the new law went into effect, and their premiums will rise, in some cases precipitously, either now, over the next several years or whenever they sell their properties. The exact amount of the increase depends on the home’s elevation above flood level.

Approved by Congress in July 2012 as part of a wide-ranging transportation bill, the Biggert-Waters Act was intended to regain control of an increasingly unsustainable National Flood Insurance Program. The subsidies within that program, in the view of critics, encouraged development in risky areas and led to costly claims after catastrophic events, payouts that were borne largely by those paying market rates.

But the effort to stabilize the program means changing rules that have guided development in flood plains for decades. Some property owners, including business owners and those who bought property after July 6, 2012, are shocked to be facing potential tenfold premium increases or, in some cases, significant losses to the value of their homes.

Property owners in the Northeast first confronted the changes as they contemplated rebuilding in the wake of Hurricane Sandy last year. But owners of flood-prone properties elsewhere are just tuning in to the changes, with many still unclear how they will be affected.

“The homeowners and business owners simply cannot withstand these gargantuan hikes,” said Senator Bill Nelson, a Florida Democrat and member of the bipartisan group of lawmakers pushing a bill to delay the increase. “There is a lot of panic about this.”

Still, in recent years, costly flooding disasters, including Hurricane Sandy, have left the program $25 billion in debt, a situation that will most likely worsen because of climate change and coastal overdevelopment. And almost everyone involved agrees that the issue is not whether to change the program, but how to soften the impact on those hit hardest by the cost increases.

“The flood insurance program is one big storm away from not existing at all,” said Steve Ellis, the vice president of Taxpayers for Common Sense, a nonprofit group that has long pushed for changes in the program. The group has suggested some measures to help those affected by the new law but insists that delays would only make problems worse. “There’s a lot of talk about fairness,” Mr. Ellis said, “but I would argue that it’s not necessarily fair that some people are paying full risk-based rates and other people aren’t.”

The alarm over the new law spreads beyond those losing subsidies to even those who intentionally built outside of high-risk flood zones and are currently paying nonsubsidized but relatively low premiums. In the past, if flood maps were redrawn and a property’s risk profile changed, the old rate was “grandfathered” in. The new law ends that practice beginning late next year. So when the Federal Emergency Management Agency recently presented revised maps for south Louisiana, the reaction was alarm.

“My whole investment premise was destroyed overnight,” said Scott Morse, who, despite being the president of a local home builders association, did not know about the changes until after he bought a new house in January.

About 600,000 homeowners nationwide will see their rates rise only if they buy new policies or allow their current policies to lapse. Homeowners are now concerned that they may not be able to sell their homes because anyone buying a property will be forced to pay the steep premiums. This has created a worrisome ripple effect in the real estate market, and some residents fear that the value of their homes has dropped.

Confronted with premiums that can range from $3,000 to $33,000 or much more, depending on the cost of the home and its risk, potential home buyers are thinking twice about properties in flood-prone areas.

The National Flood Insurance Program began in 1968 as a way to extend government insurance to homeowners in communities that tend to flood. Today, 5.5 million property owners hold federal flood insurance policies, 80 percent of whom pay market rates. Every property with a mortgage in a designated flood plain must have flood insurance, and the federal government insures a vast majority of them. In Florida, which has the most federal flood insurance policies in the country, 260,000 – or 13 percent – of them are subsidized.

W. Craig Fugate, the FEMA administrator, speaking before a Senate committee last month, said he was concerned that some property owners might have difficulty paying the new premiums, but said it was up to Congress to address that.

“I fully believe we should stop subsidizing risk as we go forward for new construction, for secondary homes and for businesses,” he said. “But I think we need to look at affordability for people who live there, look at how we can mitigate their risk.”

In some communities, like Key West and St. Pete Beach on Florida’s west coast, home sales have come to a near standstill just as the crush of the recession was beginning to fade. That could get worse when FEMA begins to phase out subsidies for condo owners in these flood zones, a decision it has put off for now.

Wendy Lockhart and her husband, who live in St. Pete Beach, a barrier island, said they recently closed on a house not too far away. Just after they put their old house on the market, they found out that for a buyer, the flood insurance rates on that home would jump immediately to $8,500 a year from $800.

“It’s a total long shot that anybody would buy this at this point,” said Ms. Lockhart, who owns a real estate brokerage firm.

Many are hoping for wealthy cash buyers who are not required to carry flood insurance because they do not have mortgages. Absent that, many are scrambling for options.

“I built to their codes, I did everything I was supposed to do,” said Claiborne Duvall, 31, who built his house outside of Houma, La., in 2011 only to find out recently that a proposed new map had moved him into a flood zone. If the map is adopted, the $412 a year he had been paying in flood insurance would steadily rise to nearly $6,500.

“What are they going to do?” he asked of those around him who could neither afford the new rates nor find someone willing to buy their homes. “Everybody’s just going to turn their keys in?”